On July 4, 2025, President Trump signed H.R. 1, the "One Big Beautiful Bill Act," into law. This legislation extends and expands key provisions of the 2017 Tax Cuts and Jobs Act (TCJA), introducing updates that impact both individual taxpayers and business owners. Here’s what self-employed pros need to know about the most impactful changes.

What Self-Employed Business Owners Need to Know About the New Tax Law

The new tax law introduces changes across both individual and business tax provisions that directly impact self-employed individuals. These modifications affect everything from your standard deduction to business equipment purchases, with some provisions offering immediate benefits while others phase in over time.

Individual Tax Changes

Several individual tax provisions in the new law will affect how you file your personal tax return, particularly around deductions and income thresholds.

Higher Standard Deduction Amounts (2025–2028)

The new tax law increases the standard deduction across all filing statuses from 2025 through 2028:

| Filing Status | 2024 | 2025 |

|---|---|---|

| Single | $14,600 | $15,750 |

| Married Filing Jointly | $29,200 | $31,500 |

| Head of Household | $21,900 | $23,250 |

In addition, taxpayers age 65 and older are eligible for a $6,000 bonus deduction. This additional amount begins to phase out for individuals earning more than $75,000 ($150,000 for married couples).

What this means for self-employed pros:

With higher standard deductions now available, more taxpayers may opt not to itemize. This may potentially reduce the impact of deductions tied to mortgage interest, charitable donations, and other expenses, a shift that may influence year-end planning and overall tax strategy.

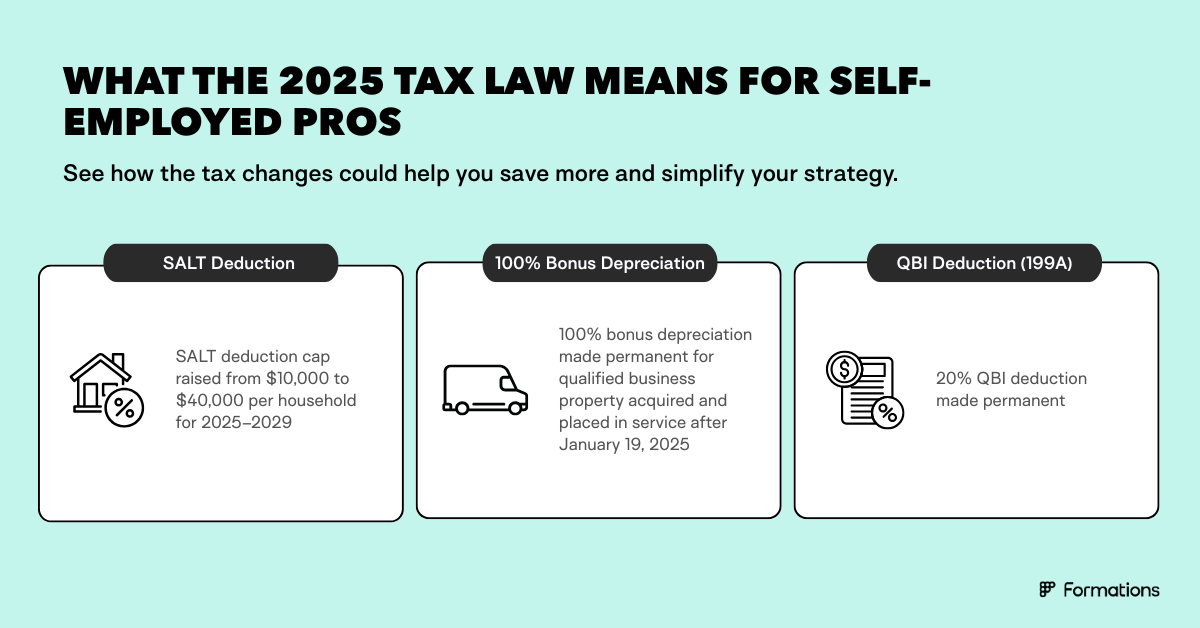

Expanded State and Local Tax (SALT) Deduction Limits

The SALT deduction cap has been raised from $10,000 to $40,000 per household for the years 2025–2029. This is a temporary change, but it offers real relief for homeowners in high-tax states.

| 2024 | 2025 | |

|---|---|---|

| SALT Deduction Cap | $10,000 | $40,000 |

Important details:

- Phase-out begins at $500,000 of income

- Both the $40,000 cap and $500,000 phase-out threshold increase by 1% annually

- Reverts to $10,000 cap in 2030

One note, the Pass Through Entity Tax (PTET) remains a valuable benefit for business owners who pay state income taxes. It allows your business to deduct state taxes as a business expense, reducing your federal taxable income. Even better, you can claim additional deductions, like property taxes sales tax, or other state taxes, on your personal return through the SALT deduction.

What this means for self-employed pros:

More taxpayers may qualify to itemize their deductions again, especially those with high state income or property taxes.

For example, a self-employed homeowner paying $12,000 in state income tax and $8,000 in property taxes was previously limited to just $10,000 total under the SALT cap. Many business owners turned to PTET elections, which allow their business to pay state taxes directly and deduct them at the entity level.

With the new $40,000 SALT cap, more of those taxes can now be deducted at the personal level — but for high earners (especially above the $500K phase-out threshold) and those in PTET-friendly states, a well-planned combination of SALT and PTET strategies may offer the best outcome.

In short:

- You deduct state taxes at the business level through PTET

- You can still take advantage of the SALT deduction personally

- Together, this creates a powerful opportunity to lower your overall tax bill.

Business Tax Changes

The bill includes several business-focused provisions that create new opportunities for tax savings and strategic planning around business investments and income.

Permanent 100% Bonus Depreciation

The legislation makes 100% bonus depreciation permanent for qualified business property acquired and placed in service after January 19, 2025. That means instead of spreading deductions over 5+ years, you can now deduct the full cost of eligible purchases in the year they’re bought.

What qualifies:

- Business vehicles, equipment, and furniture

- Computer systems and software

- Certain real property improvements

- Does NOT include buildings or land

What this means for self-employed pros:

This creates immediate opportunities for tax savings and opens the door for more strategic planning around larger business investments.

For example, a self-employed business owner purchased a $40,000 vehicle in February 2025 and uses it primarily for business. Before the new law, they would have had to depreciate that cost over five years, deducting only a portion each year.

Now, under the 2025 law, they can deduct the entire $40,000 in the year they place the vehicle in service. That means they get the full tax benefit upfront, potentially reducing their taxable income by $40,000 this year and saving thousands in taxes when the expense hits.

Permanent Qualified Business Income (QBI) Deduction

Qualified Business Income (QBI) Deduction, created by the 2017 Tax Cuts and Jobs Act (TCJA), allows eligible self-employed and small-business owners to deduct up to 20% of their business income.

Previously set to expire in 2025, the 20% QBI deduction is now permanent. The final bill also slightly loosens the wage and capital requirements for high earners.

Summary of QBI changes (starting in 2026)

| Provision | New Rule |

|---|---|

| QBI Deduction Rate | Remains at 20% |

| Expiration | Made permanent (was previously ending after 2025) |

| Wage/Capital Limitation Phase-in Thresholds | Raised by $50,000 (single) and $100,000 (married filing jointly) compared to current limits |

| Minimum Deduction | All qualifying taxpayers get at least $400 if they have $1,000+ of QBI, regardless of wages or property |

What this means for self-employed pros:

This represents the most significant benefit for pass-through entities (LLCs, S-Corps, partnerships). The permanence eliminates years of planning uncertainty, and the enhanced rate provides additional savings.

For example, before the QBI deduction was made permanent, a self-employed professional earning $200,000 through an S Corp faced the possibility of losing a $40,000 deduction starting in 2026.

Now, with the QBI deduction permanently in place, that same business owner can continue deducting a significant portion of their income with far less complexity — saving thousands each year and gaining confidence in long-term planning.

Critical Effective Dates: When Changes Take Effect

Most provisions begin January 1, 2025 and will impact your 2025 tax year filings (due in 2026). However, some key provisions have different timelines:

- Bonus Depreciation: Applies to assets placed in service after January 19, 2025

- SALT Deduction: Temporary increase through 2029, then reverts to $10,000 in 2030

Summary

Here are the top changes self-employed pros need to look out for.

Tax Planning Strategies for Self-Employed Under the New Law

If you’re not currently structured as an S-Corp:

Now may be a great time to revisit your business structure to explore whether S-Corp status could reduce your tax burden and unlock additional benefits like the QBI deduction and smarter compensation strategies.

If you’re already an S-Corp:

Reevaluate how you're approaching compensation (salary vs. distributions) and your expense planning to ensure you're maximizing tax advantages under the new permanent bonus depreciation and QBI deduction rules.

Let’s Make the New Tax Law Work for You

At Formations, we specialize in helping solopreneurs navigate tax changes, optimize their structure, and build strategies that keep more money in their pockets.

Ready to see what this means for your business? Book a free consultation with a Formations tax expert and get personalized guidance for the year ahead.